Continuing the series, this week we look at the importance of council housing delivery in London.

Whilst modest compared with some previous decades, local authority housing delivery in London has seen a small but significant renaissance in recent years, with councils such as Hackney, Camden and Croydon bringing forward highly visible programmes of development.

Recognising the momentum being developed, and with a view to diversifying and increasing the capacity of the industry, Mayor Sadiq Khan launched the Building Council Homes for Londoners programme in May 2018, handing out over £1bn to 27 councils to deliver 15,000 homes by March 2022. The funding was intended to support councils to deliver housing by:

- Developing in-house skills and expertise within councils;

- Increasing the affordable housing grant available to councils to build new homes;

- Ring-fencing Right to Buy receipts; and

- Managing additional HRA borrowing headroom.

Implementation of these measures are allowing councils to invest and grow various forms of public sector delivery including:

- Direct Delivery – The delivery of new housing through on-balance-sheet development projects, for example London Borough of Hackney's "Housing Supply Programme".

- Wholly-Owned Delivery Vehicles – A company set up by councils with the specific aim of undertaking property development, such as LB Croydon's "Brick by Brick".

- Development Partnerships – The most common form of delivery according to previous research undertaken by Future of London, Councils and development partners are brought together through a Development Agreement (or similar) to develop housing directly.

- Joint Ventures - A new public/private development company, typically set up for a specific development project or in some cases for a programme of delivery such as Southwark Council who have recently launched a search for a set up a construction company to deliver social housing across the borough.

Whilst the private sector still dominates London housebuilding, research from the GLA suggests that things are changing, council-led delivery rose 1% in FY 2017 and a further 2% in 2018. Delivery data for recent FY19 is yet to be released so we will have to wait and see whether council delivery growth continues.

Will these efforts be stalled in a 'post Covid-19' economy?

Last week we highlighted the significant challenges facing the private sector homebuilders and that they will seek various forms of intervention and flexibility from national and local government to support housing delivery.

In this context the need for public sector delivery (of all forms) will be more critical than ever to ensure that the capital recovers and continues to deliver the homes Londoners need at the pace and scale required.

However, councils themselves are also facing a number of challenges in a post Covid-19 world, including:

- Funding availability – whilst at headline level the Mayor's funding programmes such as the Affordable Homes programme, the Building Council Homes for Londoners and the Land Fund afford council's with the opportunity to access various forms of debt, equity and grant, it is clear that development economics are coming under additional pressure as a result of Covid-19, for example as proportions of more "valuable" tenures such as private sale and shared ownership reduce in response to changing market demand. The Mayor has put the case forward for more money from central government but will his voice be heard in amongst the many competing funding issues facing the Government?

- Funding milestones – Covid-19 has clearly negatively impacted delivery timescales regardless of where projects are up to in the planning and development process. Current funding milestones are typically March 2021 or March 2022; neither of which are far away in development terms. However we don't yet see a recalibration being offered by City Hall or MHCLG. We therefore anticipate this becoming an ever-increasing problem for many local authorities.

- Resource and Capacity – sufficient in-house resource, experience and expertise is often seen as a key weakness in council-led delivery. In the current climate such resource is being stretched more than ever to address the pressing frontline challenges councils are facing. Furthermore, much has been made also of the major funding shortfall facing many local authorities since the pandemic hit, which will inevitably add to the toll.

Despite this somewhat challenging context, we are observing a greater sense of optimism, determination and ambition than ever before from local authorities looking to deliver housing. Aside from addressing the obvious housing crisis, increasingly it is being seen as a vital part of economic development, linked, as it is, to wider agendas around town centres, attracting and encouraging workspace, as well as the climate emergency/carbon agenda.

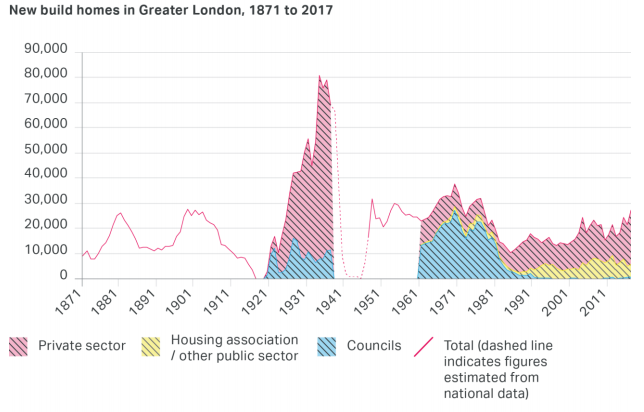

Planning for the “new normal” certainly provides a unique opportunity for the public sector to release its potential and play a greater role in the homebuilding industry. Let’s not ignore that just 40 years ago, councils built some 70% of London’s homes. Although many of those skills have been lost from council teams, building on the support given by the Mayor, with greater flexibility from national government (including promised changes to the planning system) and considered private sector partnering, we see the potential to build a small but significant renaissance in council homebuilding, into a more impactful, positive change for London.

Source: Compiled by the GLA using GLA data, MHCLG data and various other sources.

/Passle/5c9a06f6989b6e10ec2d3265/MediaLibrary/Images/2024-04-22-09-38-44-949-662630240532c9880e862159.png)